Credit Cards vs Buy Now Pay Later — Which One Is Better?

Curious whether a credit card or Buy Now Pay Later (BNPL) service is the smarter choice for your wallet? This guide breaks down the real pros, cons, and costs of each , from rewards points and fees to interest-free installments and hidden traps. Discover which option suits your spending style best in 2025 Australia before you tap, swipe, or split your next payment.

FINANCE ARTICLE

10/4/20254 min read

In Australia today, consumers have more payment choices than ever before. Two of the most common credit tools are traditional credit cards and Buy Now, Pay Later (BNPL) services like Afterpay and Zip Pay. While both let you “spend now, pay later,” their structures, risks, perks and ideal use cases differ quite a lot. Which one is better depends on your habits, discipline, and financial goals. Let’s unpack the strengths, pitfalls, and when each makes sense in the Australian context.

Why Credit Cards Have Been the Default

Credit cards have long been the go-to for deferred payments. Some of their key strengths:

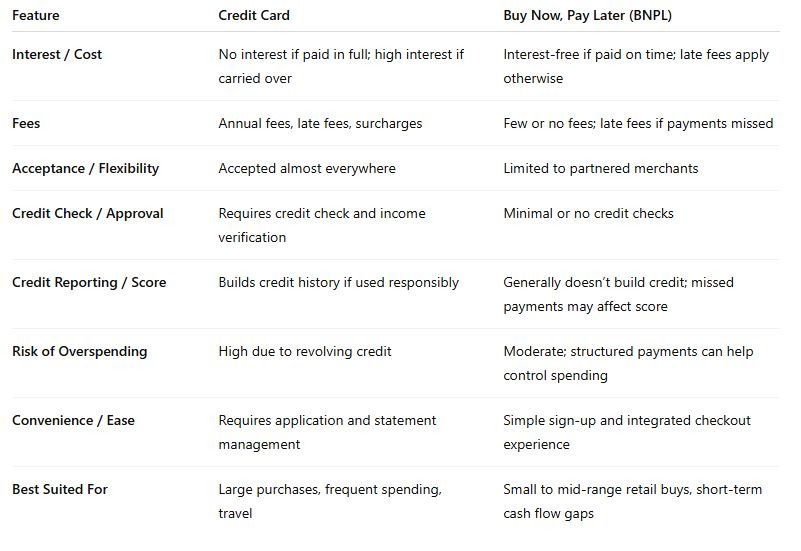

Ubiquitous acceptance: Visa and Mastercard dominate payment networks, and most retailers accept them both in-store and online.

Rewards, perks, and loyalty points: Many cards offer points, cashback, frequent flyer miles, concierge services, travel insurance, and more.

Flexible repayment and revolving credit: You can carry a balance (with interest) or pay in full each month, giving you ongoing access to credit.

Consumer protections: Credit cards are regulated and offer chargeback rights and fraud protection.

Credit history benefits: Responsible use helps you build a credit profile that supports future loan applications.

These advantages have made credit cards the backbone of consumer credit models for decades. But they’re not without drawbacks.

The Downsides of Credit Cards

High interest rates: If you don’t pay off your balance in full, interest can accumulate fast, creating debt spirals.

Annual and hidden fees: Premium cards often carry hefty annual fees, plus potential foreign transaction or late fees.

Surcharges: Many merchants pass on small card surcharges to consumers.

Temptation to overspend: Having a revolving credit limit can encourage impulse spending.

Complex interest rules: Introductory offers and balance transfers can be confusing and sometimes costly if misunderstood.

So credit cards are powerful tools — but only if used wisely.

What Is Buy Now, Pay Later (BNPL)?

BNPL is a newer financial product that lets you split a purchase into installments (often interest-free) over weeks or months. Examples in Australia include Afterpay, Zip Pay, and Klarna.

Some of BNPL’s standout features:

Interest-free (if you pay on time): Many BNPL plans don’t charge interest if you make your scheduled payments.

Minimal or no account fees: There are often no monthly or annual fees, keeping costs simple.

Structured repayments: Installments are fixed and automatically deducted, helping to enforce discipline.

Simple approval: Many BNPL providers use only soft or no credit checks, making sign-up quick and accessible.

However, BNPL isn’t risk-free — and new Australian regulations are introducing more consumer protection and responsible lending obligations.

How BNPL Providers Make Money

If you’re not paying interest or account fees, how do BNPL companies profit? Their revenue typically comes from:

Merchant fees: Retailers pay a small percentage on each BNPL sale to the provider.

Late payment fees: Missed payments trigger flat penalties, often around $10 or more.

Interest on longer-term plans: Some providers offer extended payment options with added interest.

Premium services: Optional subscriptions or “plus” accounts can include small monthly charges.

While BNPL can seem cost-free, late fees can quickly add up — sometimes becoming more expensive than small amounts of credit card interest.

Side-by-Side Comparison: Credit Card vs BNPL

When Credit Cards Are Better (and How to Use Them Safely)

Credit cards still hold strong advantages — they’re best when:

You can pay your balance in full each month to avoid interest.

You make large or irregular purchases and value flexible credit.

You travel frequently or shop overseas and need wide acceptance.

You want to build or maintain a healthy credit score.

You can maximise rewards and perks that offset annual fees.

Tips for using credit cards wisely:

Treat your card like a debit card — only spend what you can afford to repay.

Avoid cash advances and track due dates.

Choose low-rate or no-fee cards if you rarely use extras.

Regularly reassess whether your rewards outweigh the costs.

When BNPL Might Be Preferable (and What to Watch For)

BNPL shines in specific scenarios — and can be a smart tool if used carefully.

When to use BNPL:

For small to medium retail purchases you can repay quickly.

To smooth short-term cash flow without ongoing interest.

When you prefer predictable installments.

If you don’t qualify for or want a credit card.

Risks to watch for:

Late fees can add up if you miss installments.

Limited flexibility — payment dates are fixed.

Can’t be used everywhere, especially for bills or services.

Too many concurrent BNPL plans can strain your budget.

Overspending feels easier because payments are deferred.

Real-World Example

Imagine buying a $1,000 laptop.

With a credit card:

Pay it off within your 55-day interest-free period and it costs exactly $1,000.

If you carry it for three months at 20% interest, you might pay around $20 extra.

You could also earn reward points or insurance coverage, depending on your card.

With a BNPL plan:

Four installments of $250 each, no interest if on time.

Miss a payment and you could face $10–$15 in late fees.

You won’t earn rewards or build credit, but it’s simple and structured.

Both can work — the difference lies in your consistency and discipline.

Verdict: Which One Is Better?

There’s no universal winner. The “better” choice depends on how you manage your money.

Credit cards are best if you’re disciplined, repay balances in full, and want flexibility, travel perks, or to build credit.

BNPL is ideal for smaller, manageable purchases where you value simplicity and short-term structure.

Ultimately, both can coexist — many Australians use both strategically, choosing the one that best suits each purchase. The key is to see them as tools, not free money.

Tips to Use Either Option Responsibly

Budget properly — ensure you can afford repayments before committing.

Set reminders for due dates or use auto-payments.

Limit concurrent BNPL plans to avoid confusion.

Review all fees and conditions carefully.

Track your spending regularly through budgeting apps or statements.

Stay updated on regulations as BNPL laws in Australia continue to evolve.

Have a savings buffer to avoid relying too heavily on credit.

Conclusion

Credit cards and Buy Now, Pay Later services both have their place in modern Australian spending. Used thoughtfully, each offers convenience and flexibility. Misused, both can create financial stress.

Choose credit cards for long-term flexibility, rewards, and credit building.

Choose BNPL for short-term, low-cost, structured payments.

The best choice isn’t about which is “better” overall — it’s about which aligns with your spending habits, discipline, and goals.

Used wisely, either option can help you stay in control of your finances — and maybe even make your money work harder for you.

Finance & Tech Blog

Simplifying finance and tech for everyone’s understanding.

Contact Info

register below for email updates

© 2025. All rights reserved.